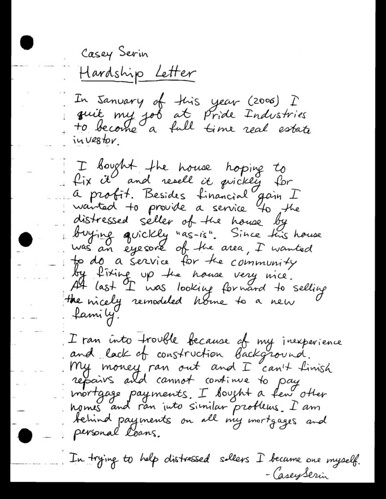

Here is my hardship letter that I wrote for asking the bank to allow a short sale on several of my upside-down properties like Larchmont and Burdett in Sacramento, and Guadalajara in New Mexico.

[See my updated hardship letter]

What is a “Short Sale”?

Sam Chapman a real estate agent from Austin puts it nicely in his Avoid Foreclosure with a Short Sale post:

This is a kind of sale that lenders may allow if a home owner is behind on payments and owes more than the market value of the home. A short sale occurs when a lender approves the sale of a property for less than market value because of a financial hardship. Lenders do not want to own real estate. They would rather take a loss on a sale than actually own the property. Lenders also don’t like to foreclose. It is a process that costs them time and money and then they are stuck owning property.

So the bank will loose a little now to avoid loosing a lot via foreclosure.

If the property is not sold via a short sale and nobody buys it at the foreclosure auction (trustee sale) then the bank automatically owns that property. At that time it’s called an “REO” – Real Estate Owned. The bank then lists the REO property with a local REO agent. The property goes on the MLS and is old in the traditional way.

Here is list of CitiMortgage REO properties. Only 6 in California?? Things must not be THAT bad yet!

The banks are not in the real estate business – they are in the MONEY business. Taking back a property creates a non-performing asset on their books. And too many non-performing assets is a bad thing.

Short Sales Increase in a Down Market.

The recent Sacramento Bee article talks about the emerging Short Sale trend (via Sacramento Landing):

Known in the real estate trade as a “short sale,” this desperate, but practical tactic — negotiating less than a complete payoff to lenders — reappears like clockwork when real estate markets sour. Widespread in Texas during the 1980s oil and real estate crash and again in the 1990s as California lost thousands of jobs to military base closings, short sales are back and proliferating, say local specialists who handled them in the 1990s. Elk Grove real estate agent Derek Kirk recently counted 264 short-sale listings in El Dorado, Placer and Sacramento counties compared with fewer than 50 six months ago…

Investors (and Banks?) Like Short Sales

John Nazareno of Foreclosure Information blog puts it this way in his Negotiating A Short Sale – The High Road To Huge Foreclosure Profits post:

The concept behind the short sale is simple: your goal as a real estate investor is to convince the bank to sell for less that is owed as payment in full. Of course, this concept is easy – buy the foreclosure from the bank at a big discount, sell the real estate, and make money!

John goes on to describe a Short Sale from a Bank’s perspective:

Short sales contracts help lenders unload unwanted property and spare many expenses associated with the foreclosure process. These expenses include, but are not limited to, court costs, bankruptcies, repairs and marketing. This is in addition to the $300,000 to $800,000 (or more!) normally held in reserve by lenders. Federal regulations require this reserve, which is usually many times over the actual price of the bad debt.

If I was the bank I sure would not want to deal with trying to sell a fixer-upper in a falling California market. They would have to either fix it up nice (banks are not in the construction business) or sit on the market for months. With so much inventory on the market the buyers are very picky. I learned first hand how tough it is to fix a property and sell quickly in this market.

Investors love shortsales because they can free up a huge chunk of equity. Nowdays a fix-n-flip investor can’t touch most properties because everybody is leveraged to the max. So once the banks becomes motivated enough to start discounting – the short sale game will begin. And it is already starting.

A true fix-and-flip investor needs to pickup the property at AT LEAST 30% off retail – MINUS repair costs. Also, hard money / private money lenders normally lend upto 65-70% of After Repair Value. So the ratio has to work for an investor before they can buy on a short sale.

I hear the banks are still letting stuff go at only about 80-85 cents on the dollar. But the ratio is dropping. Mr. Banker, do not take back that house! Sell it cheaply and quickly to an investor on a short sale. It’s Win-Win!

Short Sale Packet

The following paperwork is typically submitted to the bank by an investor (or agent) when asking for a shot sale:

- Authorization to Release Information – so the agent or investor can talk to the bank on your behalf

- Purchase Contract

- Hardship letter – personal statement by the homeowner explaining distress

- Financial statement – assets, liabilities, incomes & expenses

- Estimated HUD1 or Net sheet – showing the bank what they will get

Demonstrating Hardship with a Hardship Letter

Obviously, a Short Sale should NOT be allowed unless a borrower is in TRUE hardship. Some people might be tempted to try a short sale as an easy way to get rid of their over-leveraged property. They don’t want to come to the closing table with money out of pocket – even though they CAN.

I wish I could. I should have had some savings before starting all of my investing. I also should have been more careful with the equity I pulled out on some of the houses. If I had some money left right now, I could just drop the price and sell below pay-off. I would just have to come out of pocket at the closing table.

But instead I spent all my money on buying more properties and leveraging myself to the max. I only have myself to blame – bad planning and lack of construction and investing experience.

How to Write The Hardship Letter

The hardship letter is a personal statement from the borrower to explain the situation in “their own words”. Some say, the letter is also meant to pull at the “heart strings” of the loss mitigation agent – to make an emotional appeal.

Consider American Foreclosure Specialists’ advise on how to write a Hardship Letter:

A Hardship letter is something most Mortgage Companies will require to consider you for a “Work Out”. This is your opportunity to appeal to them to give you anther chance. This should not be used to complain to what they have done or not done to make your situation worse. This letter must be honest and represent the facts clearly. It must prove to them that the situation that caused you to fall behind was temporary and you are now in a position to make your payments on time. You must also have a legitimate excuse for falling behind… financial problems in itself would not be an adequate excuse. Loss of a job, death in the family or an illness would be an acceptable reason to fall behind on your Mortgage temporarily. We have many examples of letters that the Mortgage Company is looking for. Please contact us for a free consultation of your case.

That’s some good advice, though it’s more for the purposes of a “Work Out” – you’re asking the bank to give you another chance and keep the house. I think the same principles apply for what I am trying to do – SELL the house!

Hand-write: I wrote my letter by hand for extra appeal. Everything is computer generated now-days. A hand-written letter is very personal and should stand out from the pack.

Too Honest?

I wrote my hardship letter in a very honest and somewhat specific way. I’ve been even told that it’s too honest for two reasons:

1) Mentioning multiple properties. If the bank finds out that I have more then one property they will deny the short sale. They don’t care that I’m over-leveraged on all of them. They think if I have other property I must have at least SOME equity. “You need to sell the other houses first before asking us to take a loss”. Could this be an issue?

2) Owner Occupied Issues. I think it was an owner-occupied loan and I’m now telling them I “bought this house to fix and resell” and that I bought other houses for the same reason. Of course, there is always intent to move into the house if things don’t work out and I have to hold it. But my primary intent was to fix and re-sell. Could this cause some problems? We’ll see.

Do they even look at it?

Someone also told me that the loss mitigation reps don’t even look at the letter or my financials. They just check it off the list. They already know that I’m in distress because I’ve missed 3-4 mortgage payments. That’s proof enough. They just want to see the offer and see how much they will make. The net sheet is the only thing that matters. Is that true? Not sure… we’ll see.

Waiting for a Short Sale to be Approved…

Both of my Sacramento properties are in the middle of a short sale process.

On the Larchmont property I am working with a real estate agent who specialises in short sales. She listed the property on the MLS for a few weeks, lowering the price each week, until we got some offers.

We got two offers – 159k and 225k. The property is worth fixed up 260-280. I owe 330.

So my agent submitted the offers along with the short sale packet and my hardship letter to the first mortgage holder. We’re now waiting for a response. She says it will be 7-10 days. We’ll find out what the first is willing to take and how much they’re willing to give the second. Then we’re going to try to short sale the second. (I have a 80% 1st and 20% 2nd loan on the property).

The other Sacramento property on Burdett, is a little different. I am working directly with an investor on it. He is talking to the bank to negotiate a short sale and buy it from me. No agents involved. There is also only one loan on the property (100%).

The short sale packet has been submitted and the bank just ordered an appraisal. So the process is also moving along. I’m not sure what the purchase price is going to be yet. The investor is obvious is going to try to negotiate as low as he can to make some money.

So we’ll see which method works better – short sale via an agent or directly with investor.

I guess I could have also tried doing a short sale myself, using the knowledge from Real Estate seminars I have gone to and articles like “How to do a Short Sale” on eHow.

[See my updated hardship letter]

Are YOU Facing Foreclosure?

Did this Hardship Letter and Short Sale blog post help you?

I sure know what it’s like. I was facing foreclosure on 6 houses in 4 different states. I am still learning a lot about foreclosure, liar loans, short sales, hardship letters, and selling my house(s) fast.

Let me know if I can help you in any way… email me privately or leave a public comment below.